Credit Suisse crisis: Storm rages as bank eyes deeper restructuring, asset sales

Buckle your seatbelts...

Buckle your seatbelts...

Credit Suisse is caught up in a storm. The firm’s shares have fallen over 60% this calendar year. This morning they cratered another 9%. Late last week CEO Ulrich Koerner, who is trying to expedite an aggressive turnaround effort, wrote his second weekly missive to staff reassuring them that the bank has a “strong capital base and liquidity position”; markets are blithely unimpressed and the Credit Suisse crisis is mounting.

Over the weekend Bitcoin aficionados (many perennially keen on the rapture of financial systems collapse) and short sellers whipped up a frenzy of Credit Suisse crisis-related fear. (“Credit Suisse is probably going bankrupt. Markets say it’s insolvent and probably going bust” was one typical example.) With share prices tumbling, any capital raise on the markets is likely to be highly dilutive. Significant asset sales are on the near-horizon.

“... there has been a heightened level of media and market speculation about the potential outcome over the past days… The [Board] are considering alternatives that go beyond the conclusions of last year’s strategic review… The bank is currently executing on a number of strategic initiatives including potential divestitures and asset sales” executives said Sep 26; Bloomberg reports that sales may include its securitised products group.

Among Credit Suisse's many issues has been losses on debt racked up supporting the year's biggest US leveraged buyout -- that of networking firm Citrix. Some $4 billion in bonds backing the $16.5 billion deal to take Citrix Systems private was auctioned off in September at a 16% discount according to the Wall Street Journal. Investors had wanted far higher yields on the debt package than those that banks led by Credit Suisse had promised to private equity equity firms, leaving the banks forced to absorb sharp losses after a sharp repricing of risk assets.

The cost of insuring the firm's bonds against default (CDS) climbed some 15% last week.

Yet many market watchers say the hysteria is being overdone: “Oh my, this feels like a concerted effort at scaremongering… In 2011-2012 Morgan Stanley CDS was twice as wide as Credit Suisse is today. Take a deep breath guys” said Boaz Weinstein, Chief Investment Officer of New York’s Saba Capital Management in response to one of the many excited Tweets out there about the bank’s supposed imminent "collapse".

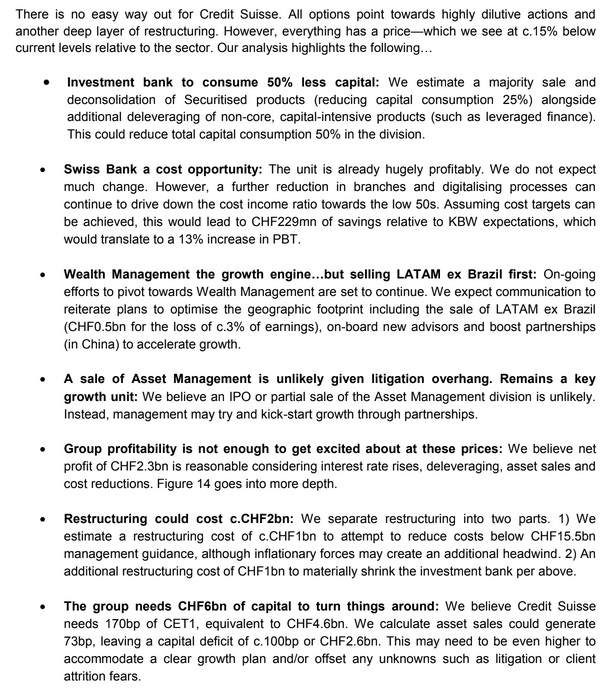

Analysts at KBW suggest that the bank may need to raise $4 billion to cover the cost of restructuring. In a report seen by The Stack they say: "We fear a negative feedback loop is now engulfing CS, similar to Deutsche Bank in 2016. In our view, replenishing the capital base, undergoing a large-scale cost reduction plan and a material shrinkage of the investment bank is the only way to stabilise investor perception and put the bank on a path to restore medium-term profitability... We see two broad-based options available to Credit Suisse:

"Option 1: CS could sell 51% of its securitisation business in order to release some capital, run down some of the IB [investment bank] and raise CHF1-2bn of capital (rather than CHF4bn). However, restructuring potential would be limited and we think insufficient to instil confidence over the medium or long term. Capital generation would be weak and the market would likely fear there could be another capital raise in the future.

"Option 2: A CHF4bn capital raise. Sell 51% of the Securitisation business, and deleverage 25% of the IB. While this would be dilutive in the near term, the extra capital allows it to materially reduce the IB, reduce the group’s risk profile and potentially provide a bit of capital to support growth initiatives" KBW's analysts suggested.

Poor risk management and inadequate systems over a long period have hurt the bank significantly.

Credit Suisse was badly exposed to the 2021 collapse of hedge fund Archegos, which cost it upwards of $5.5 billion. A July 2021 board report into its failure highlighted, among other examples, “a relatively inexpensive technology fix that had been proposed to correct for bullet swap margin erosion, but the business never executed on it” – and astonishingly how the bank in 2020 appointed a “marketing executive—with no background or training in leading an in-business risk function” to lead its pre-settlement risk (PSR) function.

A damning late-2021 report into its “hollowed out” risk function drove home that point, saying that the investment bank “failed to invest in necessary risk technology... traders [also] failed to identify significant risks, including the under-margining of Archegos swaps, and failed to perform credit checks before executing trades. As a result, traders missed numerous opportunities for action and escalation. Moreover, senior managers responsible for the business failed to challenge or escalate Credit Suisse’s increasing Archegos exposure despite weekly risk reports that clearly depicted the mounting exposure," that report added.

(In the wake of the Archegos incident Credit Suisse “immediately revised risk appetite across the portfolio”, split its Chief Risk and Chief Compliance Officer functions, completed a review of its largest clients globally, created a “dedicated Counterparty Market Risk function” -- better late than never -- among other reinforcements to both first and second lines of defence, as spelled out in a July 2022 investor day deep dive, available here.

Credit Suisse CEO Ulrich Koerner plans to deliver a revised restructuring plan on October 27.

“Some clients have used the rise in the bank’s CDS this year to ask questions, negotiate prices or use competitors, the people said, asking to remain anonymous discussing confidential conversations” Bloomberg reports, as speculation also continues that Credit Suisse could prove a takeover target for a US rival. (US market maker State Street firmly denied reports it was set to make an offer at a now-aspirational CHF9/share back in June 2022.)

More sober market observers insist the Credit Suisse crisis talk is overcooked.

"The 2025 Credit Suisse bonds pictured below trade at 6.4%. Compare this, for example to Ukraine 2025 debt trading at 67%. Talking about Ukrainian debt default makes sense. CS debt default -- less so" as analyst Alexander Good put it, adding: "CS bonds are not pricing a pending credit event because as of the July Quarter, CS's CET1 capital adequacy was at 13.5% -- within the bank's own target and well above the 8% international regulatory requirement or the 10% Swiss hurdle."

"In the pre 08' era, sub 5% CET1s were common" he noted.

Others are less sure...

On the business technology side meanwhile Credit Suisse is looking to sharply trim its $3 billion in annual IT spending and use digital transformation to help it strip $1.3 billion dollars from its annual operating expenses.

Chief Technology and Operations Officer Jo Hannaford aims to automate “[an] extraordinary amount of manual work”, outlining in June opportunities to streamline Credit Suisse’s “fragmented” IT estate of over 100,000 servers, 90,000 workstations, 37,000 relational databases, 3,000 apps and 13 data centres, and prioritise creating an “engineering, solutions-driven culture; invest in an agile talent with an engineering mindset [and] build enterprise-scale, foundational technology capabilities”, as reported by The Stack.

“Our scope includes the full bandwidth of a global universal bank for running 15 booking centres around the world for our wealth management business, processing 160 million daily client orders in our IB [investment bank] to operating 430 ATMs in Switzerland. This diversity of our business is a complexity driver, which has historically hindered enterprise platforms, front to back process harmonisation, and economies of scale. We now have one foot in the past and one foot in the future… We intend to further enhance our business platforms, enabling scalable front to back digital services, technology platforms and core capabilities.

“These are going to be best of breed technology platforms driven by our newly hired CTO, providing enterprise capabilities and savings… we are now building enterprise-scale, consistently applied foundational technology capabilities, and are making these available to business-facing engineers to deliver software quicker, cheaper, and resiliently. Hence the economies of scale being realised… These benefits should start being seen in 2024. We are funding these technology platforms in part by reducing the manual work undertaken within the technology division and repurposing this to hire more in-house engineers” Credit Suisse’s CTTO said.

Traders and others across the bank may well hope that this will also help improve risk management.

"In addition to concerns about potentially inaccurate data (in the case of potential exposure), Risk has also struggled to obtain up-to-date information on scenario exposure.

"Credit Suisse should prioritize the completion of its potential exposure remediation project, and should also ensure that credit risk management analysts have access to systems and data that allows them to run off-cycle, bespoke scenario analyses so they are not dependent on the in-business risk function for real-time information" last summer's board report on the Archegos crisis noted -- see that full report here.

Whether the firm's travails result in some form of liquidity or other crisis within the next few days or weeks appears to be a bit of an open question however. Pressure will certainly be on executives to deliver the promised restructuring plan earlier than the promised October 27 if shares continue to take this kind of pummelling.