Europe laments puny cloud presence, to crack down on foreign subsidies, boost indigenous chip capabilities.

Edge computing is place where EU could play strongly, report claims.

Edge computing is place where EU could play strongly, report claims.

The European Union has set out plans to build up capabilities in the semiconductor sector and invest further in indigenous cloud computing as part of an aggressive effort to address "strategic dependencies" and boost local capabilities in core segments. The move came as the EU updated its Industrial Strategy, and May 5 adopted a proposal to clamp down on foreign buyouts and take aim at "distortive subsidies" granted by non-EU countries.

"The EU is strongly dependent on the US for general design tools and on Asia for advanced chip fabrication. Geopolitical tensions and the lack of a level playing field harm the competition in this area", a European Commission strategic dependencies report noted, adding pointedly however that "manufacturers of chips at leading-edge nodes (TSMC, Samsung, Intel) rely for their technology development on specific EUV photolithography machines produced by a unique [European] global supplier, notably ASML..."

"The development and fabrication of chips has been increasingly subject to massive subsidies", an impact assessment (published alongside the proposed protective measures) noted, adding plaintively meanwhile that "the largest EU-based cloud provider accounts for less than 1% of total revenues generated in the EU."

The plans (set out in more detail below) come as new proposed European Commission regulations, also published May 5, give the EC the power to investigate "financial contributions granted by public authorities of a non-EU country which benefit companies engaging in an economic activity in the EU and redress their distortive effects, as relevant."

"EU rules on competition, public procurement and trade defence instruments play an important role in ensuring fair conditions for companies operating in the Single Market. But none of these tools applies to foreign subsidies which provide their recipients with an unfair advantage when acquiring EU companies, participating in public procurements in the EU or engaging in other commercial activities in the EU," a press release from the bloc said.

"Such foreign subsidies can take different forms, such as zero-interest loans and other below-cost financing, unlimited State guarantees, zero-tax agreements or direct financial grants."

The proposed regulation gives the EC the power to "impose redressive measures or accept commitments from the companies concerned that remedy the distortion [and the right to undertake a] range of structural or behavioural remedies, such as the divestment of certain assets or the prohibition of a certain market behaviour... the Commission will also have the power to prohibit the subsidised acquisition or the award of the public procurement contract to the subsidised bidder."

The EU's March 2020 Industry Strategy had already highlighted that the EU should "build competitiveness for technologies that are strategically important for Europe’s industrial future" and the May 5, 2021 strategic dependencies report re-emphases that the EU "faces particular challenges in comparison with its global competitors for technologies in the digital ecosystem such as cloud and micro-electronics."

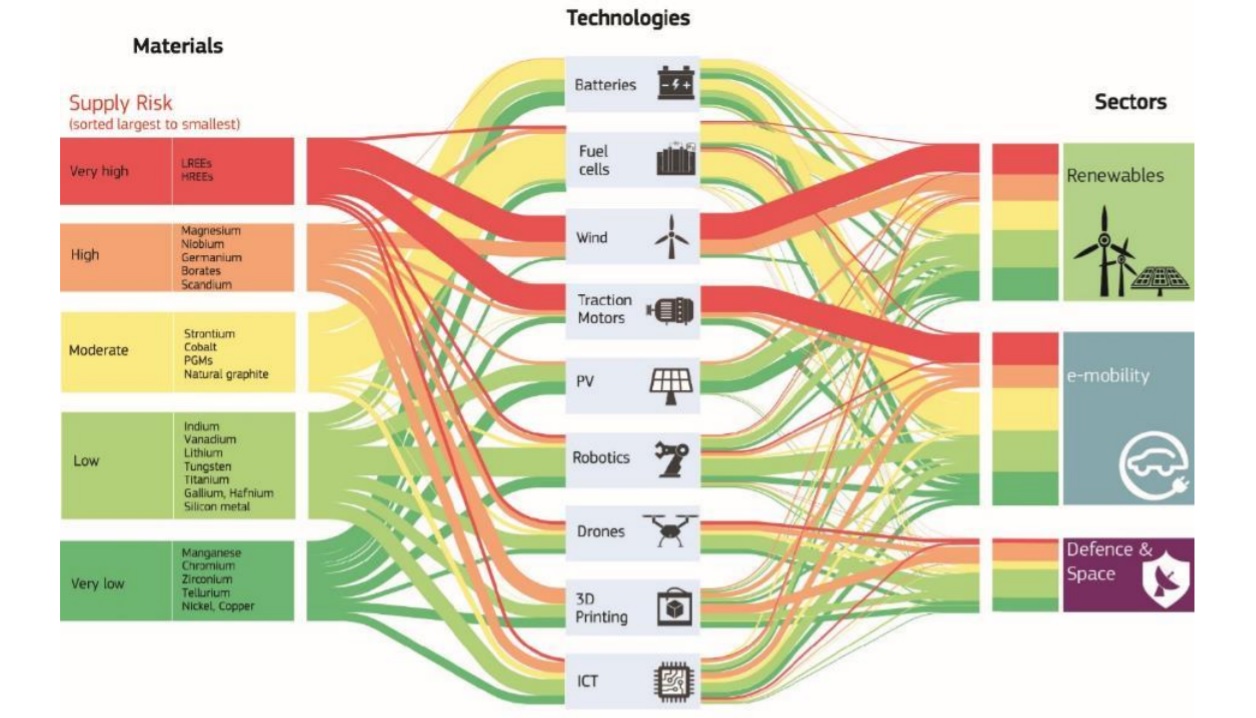

Detailing the EU's relationships with partners (and supply chain vulnerabilities) across raw materials, batteries, active pharmaceutical ingredients, hydrogen, semiconductors, and cloud and edge technologies, the report highlighted potential pinch points for critical technologies and materials. (On raw materials, China provided 98% of the EU’s supply of rare earth elements in 2020, Turkey provided 98% of the EU’s supply of borate, and South Africa provided 71% of the EU’s needs for platinum and an "even higher share" of the platinum group metals iridium, rhodium, and ruthenium.)

But a lack of semiconductor competitiveness came particularly under the spotlight -- particularly in the light of recent geopolitical tensions between China and Taiwan (a hub of high-end chip production) and moves by US President Joe Biden to take a close look at the US's own dependencies.

"The EU appears to be facing challenges compared to its global competitors (e.g. cloud, semiconductors)... Europe has no foundries that offer manufacturing of components with feature sizes below 22nm" the report notes, adding that "with high entry cost, escalating trade tensions and subsidies at global level, dependence on Asia for advanced chip fabrication and on the US for chip design tools, the EU supply chain is left increasingly vulnerable. Europe needs to strengthen its own industrial position to minimise risks from trade disruptions and boost innovation and competitiveness in the application sectors."

Only 36% of EU enterprises used cloud services in 2020, mostly for simple services like e-mail and storage of files -- May 2021 Strategic Dependencies report.

Commissioner Thierry Breton, responsible for the Internal Market, said: “The real industrial revolution is starting now – provided we make the right investments in key technologies and set the right framework conditions. Europe is giving itself the means for an innovative, clean, resilient industry which provides quality jobs and allows its SMEs to thrive even during the recovery process.”

"Joint European actions and initiatives will need to strongly focus on rebuilding capabilities in processors and semiconductor technologies critical to enable powerful and energy-efficient data processing, communication, infrastructure and the many applications of AI," the European Commission concluded, adding that semiconductors are "among the areas identified for investment" under its €672.5 billion Recovery and Resilience Facility.

(As the EC points out pithily, "a new fab with the latest technology is challenging both technologically and economically (EUR 20bn upfront and EUR 5bn p.a. to operate) and is not in the reach of any individual EU supplier today.")

"A coherent mix of industrial, research and trade policies can facilitate the process of diversification to alternative sources of supply and strengthen the existing supply chains through partnership and collaboration with global partners, it concluded.

Efforts are already underway to try and create a European cloud ecosystem under the Gaia-X rubrik, but this week's set of papers reiterates how much of a sore spot EU underperformance in this area is chastening policy makers. It's not just lack of a market champion, however: adoption remains minimal. According to Eurostat’s data, while improved compared to 2018, only 36% of EU enterprises used cloud services in 2020, "mostly for simple services such as for e-mail and storage of files", the strategic dependencies paper notes.

The largest EU-based cloud provider accounts for less than 1% of total revenues generated in the European market. "In comparison, the top four global leaders (Amazon Web Services, Microsoft Azure, Google Cloud and Alibaba Cloud) will account for over 80% of global revenues in 2021. The market position and scale of these hyperscalers makes market entries by other competitors less rewarding and prevents the rise of European leadership," the EC lamented, adding that the situation is "exacerbated by an estimated investment gap of €11 billion annually between what the US and China and the EU invest in cloud."

A strong European presence in micro-controllers for embedded systems, industrial uses, and the fact that "EU industry is for now less dependent in the currently nascent edge computing segment" gives some pointers for European policy makers, the review concludes: "[This] constitutes the best opportunity for Europe to revert today’s cloud market structure and regain autonomy in a market dominated by non-EU providers. European focus could also be on supporting the emergence of smaller providers at the edge market and their growth, in order to prevent the situation where a few big actors dominate this market."