Cloud

Satellite data infrastructure provider Ursa Space capped off a busy few months for the company today by announcing it had raised $16m in Series C funding from several big-name investors.

Last November, meanwhile, the firm became an AWS Partner; then on 12 January Ursa Space said it was working with AWS Data Exchange to make its data available to cloud users as a service.

These moves estalish the seven-year-old firm firmly within a new generation of geospatial data service enterprises – a group that has, somewhat inevitably, been dubbed Geospatial 2.0. (Among the customer use cases for Ursa Space are analysis of disruption near utilities' pipelines and analysis of oil inventories using a combination of synthetic aperture radar imagery of oil storage sites and data visualisation techniques.)

Until the last few years, serious use of geospatial data was mostly limited to governments and major enterprises. But the proliferation of satellites providing high-quality data at increasingly lower costs, along with the growth of other sensor data at ground level, has opened up new possibilities across multiple verticals.

“In recent years, the field of geospatial analytics has emerged at the intersection of GIS, artificial intelligence (AI), and cloud- based computing,” says Josh Gilbert, CEO of climate data firm Sust Global, in a 2020 report from Ordnance Survey and KTN, adding: "We have seen an evolution from a collection of tools for analysts to download, view and analyse, towards a scalable collection of cloud native capabilities that promise to deliver action-oriented insights to decision-makers across multiple industries.”

That report cited research suggesting the global geospatial data market could see a CAGR of 14-17%, growing to around $86 billion by 2023. A UK government report from late 2020 meanwhile gave a “conservative estimate” of £6 billion for the value of geospatial-related turnover in the country in 2018, excluding large tech firms such as Google and Apple.

See: Apache Sedona: ‘Big Data’ meets geospatial data

“While there has been an initial focus on ‘low-hanging fruit’ applications, such as precision agriculture, finance and defence, there are huge markets where uptake of geospatial products will drive billions of dollars in value, ranging from insurance, climate change, supply chain management and intelligent city management,” adds Gilbert in the OS/KTN report.

The challenge is in ingesting, cleaning and harmonising the data for easy use – which is where players like Ursa Space, and competitors such as Descartes Labs, Orbital Insight and Remote Sensing Metrics, come in.

They join establised providers of GIS data such as Esri, which has partnered with IBM for its ArcGIS - and which is also moving to a PaaS model for accessing its data via API.

These firms claim to provide anything from raw image data, to images showing arrivals or departures of objects from a location, to industry-specific information such as car production numbers.

“We’ve made tremendous progress … by eliminating many of the barriers that people faced when trying to get answers from satellite imagery. In its place, we’re building the infrastructure that enables a community of developers to form and create new services that improves understanding of what’s happening on earth,” said Ursa Space CEO Adam Maher in a press release announcing its latest funding.

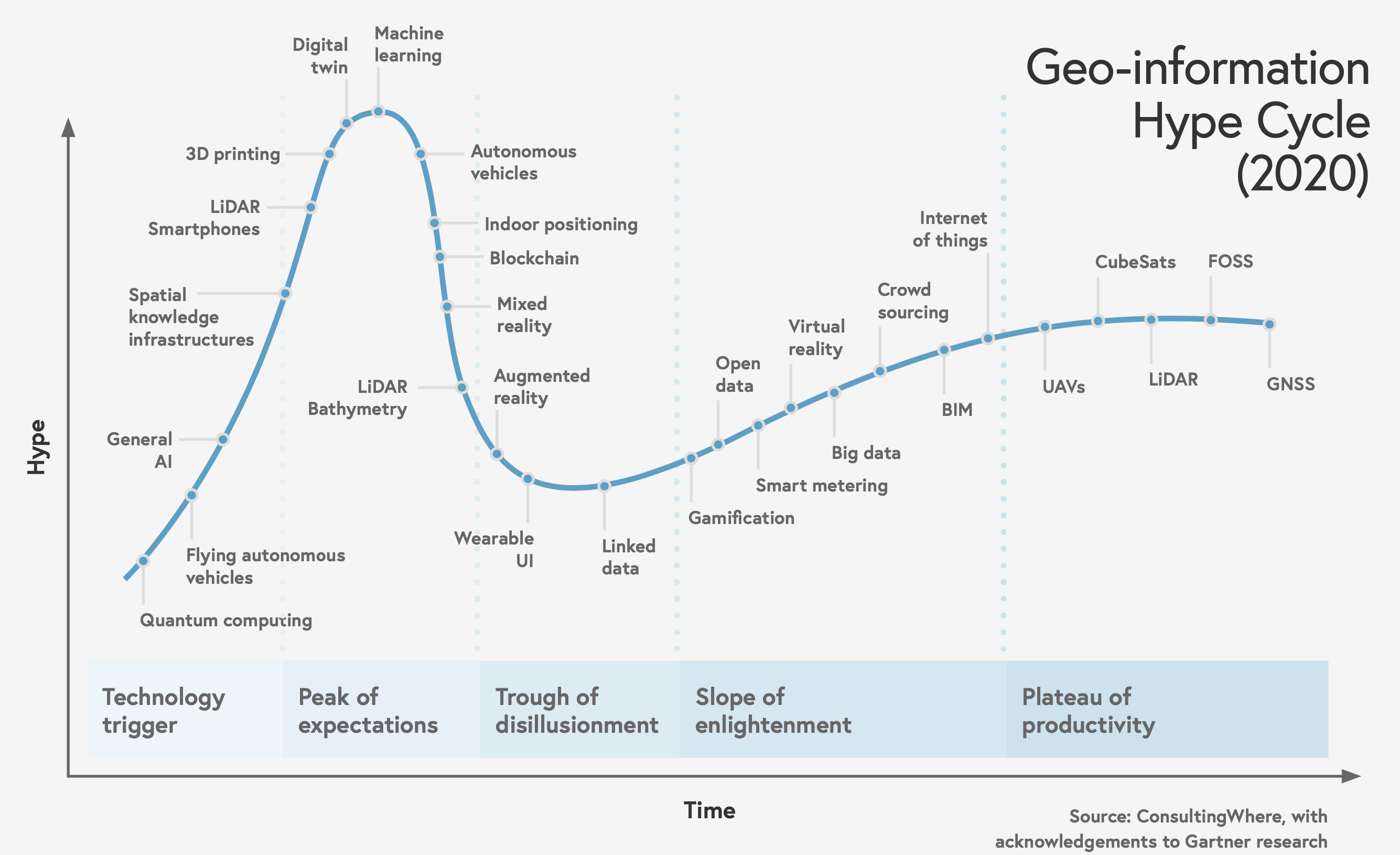

But there is still a long way to go before some of the promises of geospatial data are fully realised. ConsultingWhere produced a version of Gartner’s Hype Cycle focused on geo-information applications, and it’s clear from this how many use-cases are still facing a slow journey through the trough of disillusionment.

“The challenge for PaaS providers to date has been that in order to serve a wide collection of use cases, there exists a technical gap for harmonising data from multiple sensors together (a sensor fusion problem) and a solutions gap to address different forms in which insights can be consumed (an integration problem). These two issues can be broadly characterised as a technological problem, and a business model problem, respectively,” says Gilbert.

Dr Lesley Arnold, CEO of Geospatial Frameworks in Australia, described the change that needs to happen as a shift to the “semantic web” in a presentation at Norway’s mapping authority Kartverket’s annual conference in October 2021. She describes the need for a “spatial knowledge infrastructure” (SKI).

She defines an SKI as: “A network of data analytics, expertise and policies that assist people, whether individually or in collaboration, to integrate in real-time spatial knowledge into everyday decision-making and problem solving.”

The model Arnold describes is complex, and requires a lot of development in both machine learning and data processing. According to her estimate, it could take until 2025 to realise the full vision of an SKI, and this will require significant work beyond just the technological challenges.

Follow The Stack on LinkedIn

The good news is the current generation of geospatial data is opening up more and more opportunities, for users at every level. One of the examples given in the OS/KTN report is of data from the European Sentinel satellite system, which has been made available to use for free, for both businesses and researchers.

“The data-driven agriculture company OneSoil is an example of both service and product innovation that has benefitted from open data,” says Aleks Berditchevskaia, senior researcher at the Centre for Collective Intelligence Design, Nesta, in the report.

“They offer an integrated predictive analytics and decision making platform that helps farmers across the world better manage their crops and coordinate with their teams. Their platform identifies field boundaries and monitors crop health using data derived from the free Sentinel satellite images in combination with data from in-situ sensors contributed by farmers.”

Moving to cloud infrastructure has been a game-changer for many industries, and by opening up previously siloed geospatial data and providing it as an easily accessible service, the Geospatial 2.0 movement may well provoke a similar shift for this data.