Sponsored - You may not have heard of Banking Circle. Yet despite the comparatively low brand visibility, Banking Circle settles 10% upwards of the world’s total ecommerce payments, including for household names like Alibaba, Shopify, and Stripe, while a growing number of high profile customers quietly use its infrastructure and services for their banking, payments settlement and other financial services around the world.

So what exactly is Banking Circle and how does it fit into a rapidly evolving financial services ecosystem? The Stack sat down with CEO Anders la Cour to find out more about the rapidly growing company.

A Bank, a platform, a utility… what is Banking Circle?

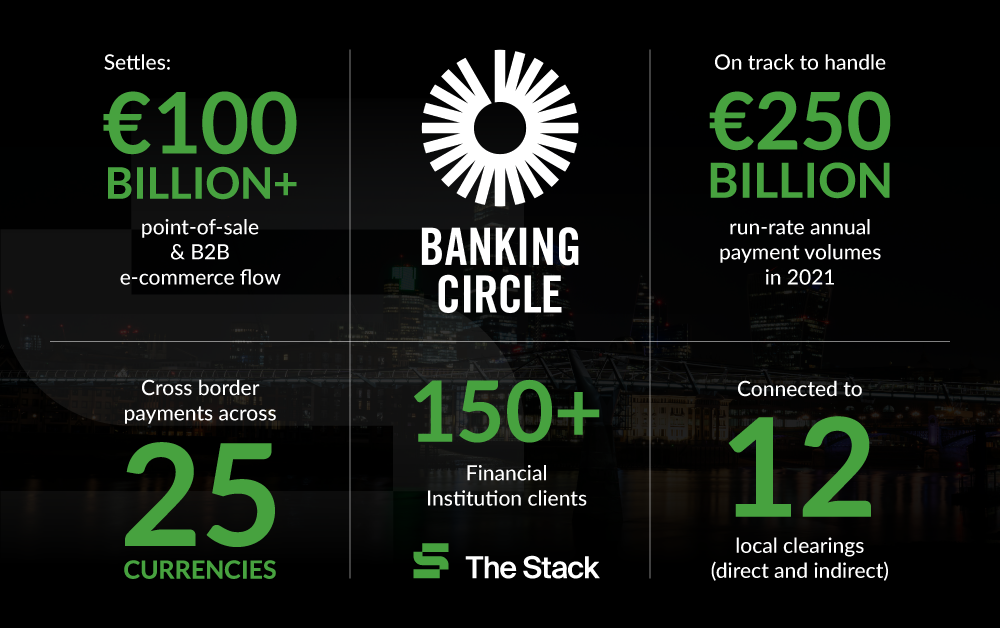

Banking Circle, founded in 2013 and acquired by private equity firm EQT in 2018, is a fully-clouded scalable financial infrastructure provider building the first and only real-time clearing and settlement network globally. It can run white-labelled current accounts, payments, settlement, and FX underpined by strong compliance services for customers on its own cloud-native and open API-powered infrastructure.

It is on track to handle $250 billion in payment volumes annually in 2021 for 150+ institutional clients. It is connected to 12 local clearings and offers cross border payments in 25 currencies.

In 2020 Banking Circle received a full banking licence in Luxembourg that also allows it to offer financial institutions and large corporates the ability to offer banking services such as cross border payments, multi-currency accounts and FX to their merchant clients. The timing is perfect: many banks are rethinking their branch footprint and streamlining operations; the ability to task a partner with running the back-end of multiple financial services is a compelling one: Banking Circle doubled its customer base after securing the licence and is on track to provide an estimated 100 million bank transfers in 2021.

With the banking licence acquisition has come the ability to offer Banking Circle safeguarded operational and settlement accounts to corporates and regulated entities for their operational and treasury business needs – i.e. customers get a physical account held in the name of the corporate that can be linked to underlying virtual IBANs to allow department, entity or operational reconciliation, without the need for multiple “actual” bank accounts in multiple geographies. (Customers can choose to view the account either online or via an API, Banking Circle says.)

As CEO Anders la Cour puts it: “Where we have a sweet spot for banks is that operating different branches in multiple countries is becoming more cumbersome, due to compliance and increased regulatory burden. If you have a branch in a specific country, you also need to report; to have staff: there's lot of costs associated with operating a branch. Many mid-sized banks particularly that are seeing increasing competition in their core markets are retrenching from branches - but still need to service large corporates in these countries.

“Take for example a Swedish bank that is servicing some of the largest Swedish corporate clients. If they stop operating their branch in, say, France, that particular corporate cannot be serviced without local banking services in France. That is where we come in: but we can do it behind the scenes, so the corporate gets exactly the same feeling and service, but the bank will have reduced its overhead and its complexity.

“Again, imagine you are an English bank: you have a corporate customer (call it Corporate #1), selling shoes in Germany, which would really like its suppliers in Germany to pay into a local German account. We set up a German account in the name of Corporate #1 for the English bank. Corporate #1 can give the account number to the supplier, and the second the supplier pays into that account, it goes automatically to the account that you have in your control as a bank. We’ve created a kind of ‘mirror’. And now irrespective of currency, the money will end up where it was supposed to end up. This gives banks a lot of flexibility.”

CEO Anders la Cour draws a compelling parallel: “It’s like the beginning of the Industrial Revolution right now, when a lot of people trying to build their own factory put their own power generator in the backyard. At some point, they realised trying to rely solely on their own generator was expensive, and dangerous. We are at a similar moment in financial services where banks are recognising it is better to get a power supply, plug into it, and then do what you do best as a bank, and focus on service innovation.”

Are banks not reluctant to relinquish control over such core services, The Stack asks: what about losing visibility, resilience; a sense of ownership? Banking Circle CEO Anders la Cour says the short answer is no.

“Most currently struggle for visibility into their data. We’ve been privileged to build our bank ‘after compliance was invented’; to build in a way that reduces resource needed to identify transaction laundering and lower risk. So we actually offer improved data visibility and compliance for our customers, while reducing risk.”

He adds: “Banks and tech companies are now all fighting for the client. As a partner at Anderson Horowitz has noted, soon every company will be a FinTech company, meaning that every company will try to monetise on their client base by selling client services; the lower part of the value chain, the infrastructure piece, will continue to be commoditised – because the higher margins for banks and corporates are in other parts of the value chain. They don't need heavy financial infrastructure in all places. And that’s where we can help.”