Cloud

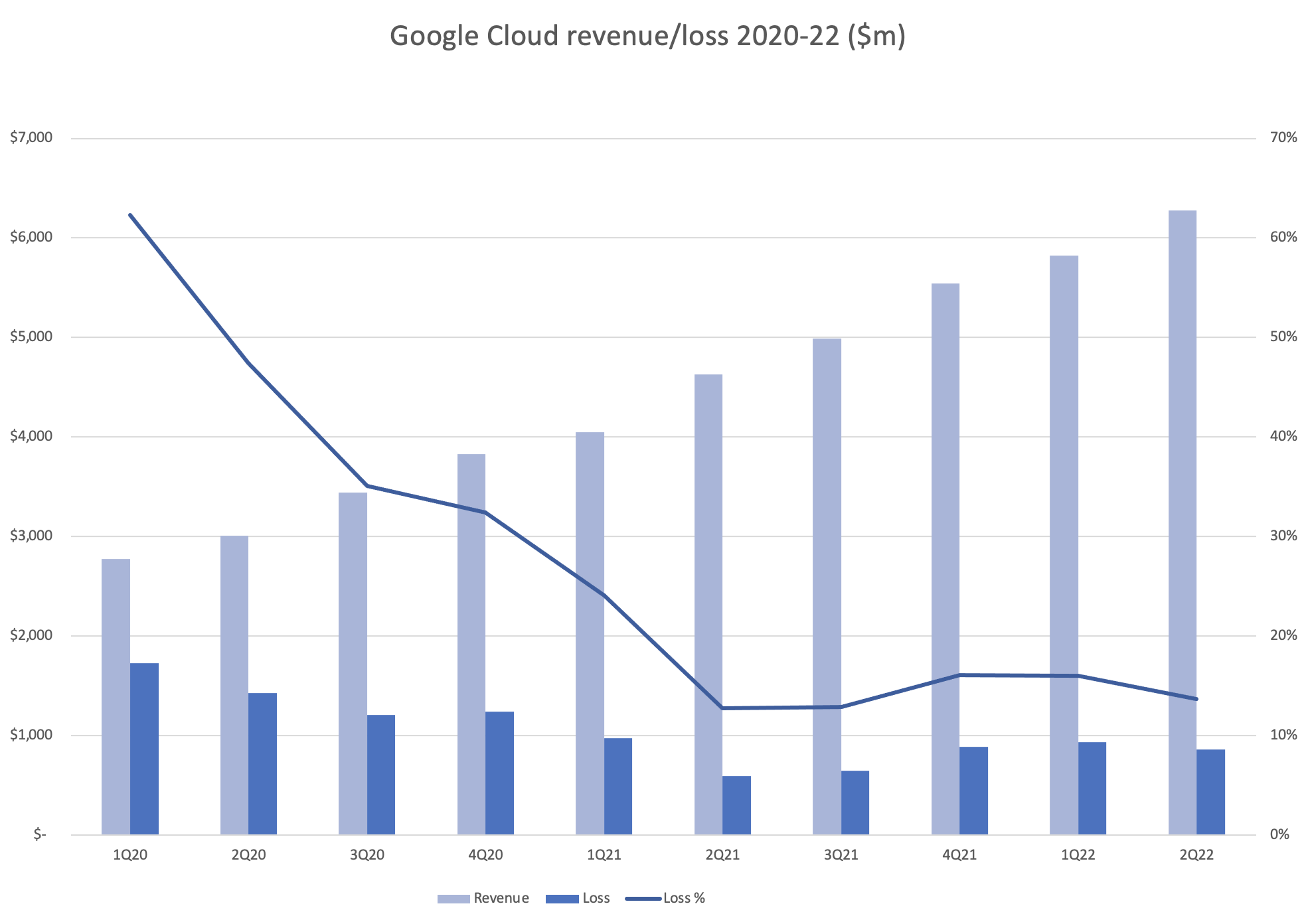

Google Cloud revenue was up, but losses widened by 45% year-on-year in Q2, as the search and advertising giant struggled to expand its cloud market share – but bosses remained upbeat about its future.

Alphabet’s Q2 earnings, announced 26 July, revealed Google Cloud revenue grew 36% compared to Q2 2021, reaching nearly $6.3 billion for the quarter. While cloud is a massive profit-generator for rival hyperscaler AWS, at Google, cloud losses grew to $858 million, largely on Google’s increased spending on data centres.

CFO Ruth Porat said Alphabet’s biggest Q2 investments were in data centres (along with office facilities, presumably for Google’s return-to-office plan, which has seen mixed results). She also said part of the reason for the jump in cloud costs was a “lag” on data centre investments, which pushed the costs later on in the year.

But even with Google Cloud revenue growing and loss rate holding reasonably steady over the last year, at 13-16% of revenue, its investments in the cloud business only seem to keep it treading water.

While Google Cloud revenue grew 36% in Q2, Microsoft Azure revenue climbed 40% in the same period (46% in constant currency terms) – and in Q1 AWS grew 37% (Amazon’s Q2 results are out tomorrow).

See also: Microsoft layoffs cost it $113m in Q4: That’s 5 hours’ earnings

Not only are AWS and Azure five times the size of Google Cloud in revenue terms, but both appear profitable – in AWS’s case, wildly so. (We should note Microsoft does not break out Azure’s actual revenue or profit/loss figures, but bundles it into its “commercial cloud” figures, which include Microsoft 365, LinkedIn and other money-spinners – a lack of transparency which has been repeatedly called out by analysts and journalists alike.)

Alphabet’s management has brushed away these concerns, stating they are investing in the long-term potential of the cloud market.

“On Cloud, we continue to see strong momentum, substantial market opportunity here and still feels like early stages of this transformation. Constantly in conversations with customers, big and small, who are just undertaking the journey. So it kind of shows you the opportunity ahead,” said Alphabet CEO Sundar Pichai during the Q2 earnings call.

In answer to a question about Google Cloud revenue and the urgency of moving towards break-even, Porat said: “It's a long-term opportunity and enterprise customers are still early in their move to the cloud. And so, we do very much have that debate, that same question that you posed is the right one, which is a trade-off as between revenue growth and immediate profitability.”

This is fine as far as it goes, and Google’s other revenue streams – it turned a $16 billion profit for the quarter, on the back of nearly $70 billion revenue – means it can support Cloud for some time to come. But again, given AWS has been Amazon’s main profit driver for years, Google’s lack of headway into the cloud segment could be a cause for concern.

Alphabet’s ‘Other Bets’ losses widen

To put Google Cloud’s $858 million loss in perspective, Alphabet’s “Other Bets” segment – covering its experimental projects – booked a loss of nearly $1.7 billion in Q2, up 20% from Q2 2021, and up 45% from Q1 2022. Revenue from these was $193 million less than half Q1’s $440 million.

Other Bets includes projects such as autonomous vehicle division Waymo, drone operation Wing, and health research operation Calico. Alphabet’s earnings release describes Other Bets revenue as being “primarily from the sale of health technology and internet services”.

Since its creation in 2015 the Other Bets division has been a bit of a hot mess, with companies being moved around, renamed, and occasionally shut down. In comparison Google Cloud is a well-oiled machine, well on the path to commercial viability.