The first big software deal of 2023 is in, with Progress agreeing to buy NoSQL database and metadata management company MarkLogic for $355 million. Despite sitting in the Gartner Magic Quadrant for Cloud Database Management Systems with the hyperscalers, MarkLogic has low visibility, but a reputation for unique “data agility” capabilities, a sticky blue chip customer base (Airbus, J.P. Morgan, Nike, Merck) and a strong reputation for customer service: Customers will be hoping that the latter continues post-acquisition.

MarkLogic describes itself as a “multi-model database” that combines document, semantic graph, geospatial, and relational models (native storage for JSON, XML, text, RDF triples, geospatial, and binaries (e.g., PDFs, images, videos) into a single, scalable, high-performance and ACID-capable operational database. The company cites “a major investment bank” as a key customer (we’d speculate wildly that this is J.P. Morgan) which uses it to underpin its derivatives trade store and swapped out a total of 20 Oracle and Sybase databases for MarkLogic.

Progress agrees to buy MarkLogic: A little about both

Progress, listed on the Nasdaq, is a large provider of application development and infrastructure software, with over 100,000 enterprise customers and more than 2,000 employees in 20+ countries. It expects the deal – which executives said would give it a “best-in-class, proprietary, multi-model NoSQL database, along with robust semantic metadata management and AI capabilities” -- to add $100 million in ARR to its bottom line.

MarkLogic, in the "visionaries" corner... Credit: Gartner

MarkLogic positions itself as a NoSQL database system for integrating data from various data silos and improving “data agility”. It was last year named a visionary in its Magic Quadrant and made a significant acquisition itself in November 2021 with the buyout of metadata management firm Smartlogic.

MarkLogic’s revenues appear to have stagnated at around $100 million for some years, but it has been innovating hard regardless, recently for example adding tools that support the indexing and querying of geospatial data, scalable export of large geospatial result sets, and interoperability with GIS tools.

CEO Jeff Casale told staff: “Progress understands the value MarkLogic brings to the database and semantic metadata management customers. It will bring significant cross-functional corporate resources to bear in securing the long-term success of our customers and our people.”

They would be forgiven for feeling just a little twitchy at Progress’s comments to investors that the deal is “expected to provide an opportunity for Progress to leverage its highly disciplined operating model and infrastructure to maximize efficiency”. Watch this space to see how that pans out.

Progress MarkLogic deal: A sign of deals to come in 2023?

The acquisition as 2023 barely gets warmed up may be a sign of things to come.

As EY suggested in late 2022 “faced with high inflation, an energy crisis and falling consumer confidence, the biggest opportunity for tech companies in 2023 is to adopt an active M&A strategy.”

As EY's Olivier Wolf, a Global TMT Strategy and Transactions Leader, put it on December 7: "The deal market has slowed due to macro headwinds and financial volatility, but this has improved opportunities for corporate buyers with strong balance sheets. In turn, competition for targets should heat up again next year, as hundreds of billions of private equity dollars come to the market. Transformative acquisitions could launch tech companies into new markets or adjacent verticals like HealthTech, and accretive acquisitions have the potential to strengthen portfolios with leading-edge technologies like artificial intelligence.”

One observer of the database market suggests bumpy times ahead after rampant raising in 2021.

Dr Andy Pavlo, Associate Professor of Databaseology (really) in the Computer Science Department at Carnegie Mellon University and co-founder of OtterTune, a database tuning company, noted in a thought-provoking blog at the close of 2022: "The bad news is that these companies [DBMS startups] are in trouble unless the tech sector improves and big institutional investors start turning their money out on the street again.

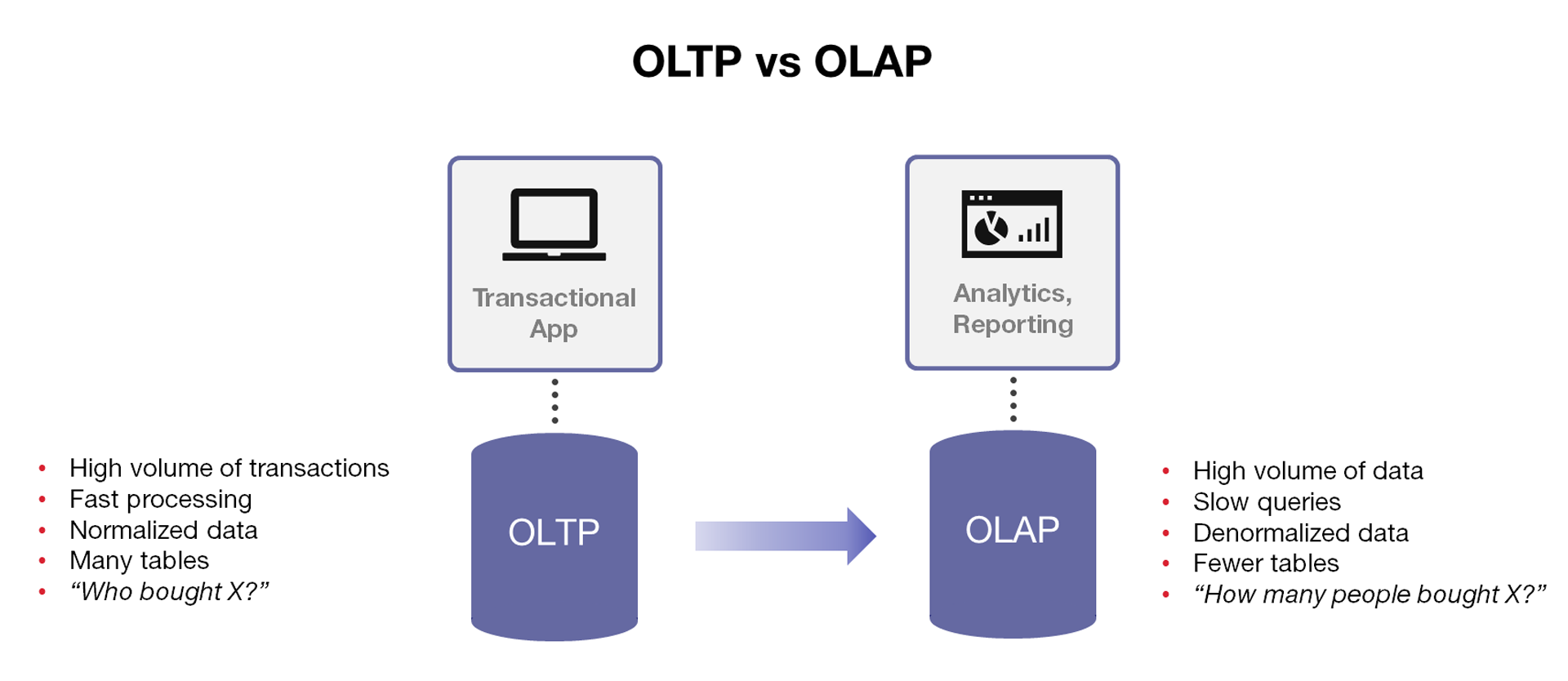

"The market cannot sustain so many independent software vendors (ISVs) for databases... They are too expensive for acquisition (unless the VCs are willing to take massive cuts) for most companies. Furthermore, the major tech companies (e.g., Amazon, Google, Microsoft) that do large M&A’s already have their own cloud database offerings. Hence, it is not clear who will acquire these database start-ups. It does not make sense for Amazon to buy Clickhouse at their 2021 $2b valuation when they are already making billions per year from Redshift. This problem is not exclusive to OLAP [online analytical processing] database companies; OLTP [online transaction processing] database companies will face the same issue soon.I am not the only one making such dire predictions about the fate of database start-ups."

"Gartner analysts predict that 50% of independent DBMS vendors will go out of business by 2025. I am obviously biased, but I think the companies that will survive will be the ones that work in front of DBMSs to improve/enhance them rather than replace them (e.g., dbt, ReadySet, Keebo, and OtterTune)," he added.